Your Guide to Open Banking

Date: 15 January 2025

Reading Time: 5 minutes

Your Guide to Open Banking

Even when using a contract, we know that many find the payment to be the scariest part of buying or selling something online. Does the buyer pay first or does the seller hand over the item? Is there a way for both parties to be safe?

Yes! Open Banking can provide a framework for ensuring safety and transparency in transactions for both parties.

In this blog post, we'll take an in-depth look at Open Banking, exploring how it works, the benefits it offers to banking customers and learn a bit more about how we use Open Banking at Swiftcourt.

Here is what you’ll learn reading this blog post:

- What is open Banking?

- Benefits of Open Banking

- Open Banking Provider

- What is Escrow?

- How do we use Open Banking at Swiftcourt?

- Conclusion

Let’s dig in!

What is Open Banking?

Open Banking is transforming how consumers interact with their financial services, making it easier to access and manage their finances, while also enabling greater innovation in the financial services sector. Open Banking is built on the principle that financial data belongs to the customer, and they should have the freedom to use it to their benefit. By fostering collaboration between banks and third-party providers (TPPs), it creates an ecosystem where customers can leverage their financial data to access improved products and services.

This shift allows tech companies to access banking information with customer consent, fostering competition and helping to reduce costs. But Open Banking is more than just a technological trend - it’s transforming our relationship with money. As banks and fintech companies collaborate, we can expect more personalized, efficient financial products that cater to our unique needs.

Benefits of Open Banking

Open Banking creates a more transparent, competitive, and customer-centric financial system, offering significant advantages such as better control over data, personalized services, faster transactions, and improved financial inclusion. It’s paving the way for a more dynamic and innovative financial future.

Open Banking allows your bank to securely share your financial data with TPPs. This helps you access new financial services or products, often through apps or websites that can make managing your money easier. This means that a TPP could use open banking to enable direct payments from a bank account to a merchant.

Open Banking also facilitates faster and cheaper cross-border payments, reducing transaction costs due to low transaction costs for bank transfers compared to high transaction fees for card payments.

At Swiftcourt we have combined the benefits of Open Banking with an escrow solution (further described below) to make our payment service as secure and smooth as possible.

Open Banking Provider

An Open Banking provider is any bank, fintech company, or payment service provider that facilitates the secure sharing of financial data and services via APIs (Application Programming Interfaces), empowering consumers with more control and access to innovative financial solutions.

Examples of some of the biggest Open Banking providers are companies like Plaid, TrueLayer,

Tink, and Yapily, which all provide APIs to enable secure access to financial data. These

platforms are often used by fintech apps, lenders, and other digital finance companies to offer

services such as budgeting, payments, lending, and investment advice.

Examples of some of the biggest Open Banking providers are companies like Plaid, TrueLayer,

Tink, and Yapily, which all provide APIs to enable secure access to financial data. These

platforms are often used by fintech apps, lenders, and other digital finance companies to offer

services such as budgeting, payments, lending, and investment advice.

TINK

At Swiftcourt we use Tink as the Open Banking provider. Based in Stockholm, Tink supports banks and fintechs across the continent by providing APIs that allow users to connect with over 3,400 banks. Tink’s platform offers transaction data, account balances, and payment capabilities, helping businesses develop innovative financial products and improve user experiences. Tink is responsible for providing Open Banking services, Application Programming Interface (API), Payment Initiation Service (PIS) and Account information Service (AIS) (further described below).

Application Programming Interface (API)

In the context of Open Banking, an API (Application Programming Interface) is a crucial

tool that enables secure, standardized communication between banks, third-party

providers, and other financial services. You can say that API is the backbone of Open Banking,

enabling secure, standardized communication between banks and third-party providers.

Open Banking providers (whether they are banks, fintechs, or other financial institutions)

use APIs to open up access to financial data and services in a way that is secure, efficient,

and customer-centric.

Account Information Service (AIS)

An Account Information Service (AIS) is a financial service that allows businesses or

individuals to access and view consolidated information from multiple bank accounts in one

place. Regulated under frameworks like PSD2 (Payment Services Directive 2) in the EU, AIS

retrieves account data securely with user consent, helping users gain better insights into their

financial activities without storing or processing the data beyond its retrieval.

Furthermore, AIS also allows the supplier to retrieve information about the seller and the

seller’s bank account necessary to perform the required KYC (“Know you customer”) on both the

seller and the buyer. AIS helps ensure that financial information is recorded accurately.

It is highly regulated for security, and is designed to give consumers greater control and

visibility over their financial data.

Payment Initiation Service (PIS)

PIS stands for Payment Initiation Service. PIS is a third-party service offered by the Open Banking provider (Tink), that allows a Buyer to authenticate towards his/her bank and initiate and confirm online payments from a bank account into another bank account, for example, an escrow account. In online transactions, this ensures a smooth and secure user experience allowing the buyer to confirm payments without having to leave the website where they are conducting the transaction. PIS is also regulated under PSD2 (Payment Services Directive 2).

What is Escrow?

Escrow and Open Banking can work smoothly together to enhance security, streamline payments, and improve transparency in financial transactions. But what is Escrow?

Escrow is a financial arrangement where a third-party service temporarily holds funds or assets during a transaction between two parties. The purpose of escrow is to ensure that both the buyer and the seller fulfill their obligations before the deal is finalized. If everything goes according to plan, the funds or assets held in escrow are released to the appropriate party. If not, the escrow agent will follow the agreed-upon instructions, often involving a refund or dispute resolution. Click here to read our help center article about Escow and have a look at our other related articles.

At Swiftcourt we use Ping Payments as the processor (host) for the escrow account. Ping is also responsible for any related services, such as Payouts and Refunds. As a licensed financial institution under Finansinspektionen, Ping Payments meets all the requirements to keep the money safe until the transaction is completed.

Why Use Escrow?

- Protection: It protects both parties in a transaction, ensuring neither the buyer nor the seller takes on unnecessary risk.

- Trust: It helps build trust between people who may not know each other well, especially in big transactions.

- Dispute Resolution: If there’s a problem or disagreement during the deal, the parties can get help mediate or hold the funds until the issue is resolved. Click here to read more about Swiftcourt Dispute Assistance

How do we use Open Banking at Swiftcourt?

With Open Banking we have created a digital payment solution that makes the payment simple and secure for both parties. When you use one of our contracts you can choose to use our secure payment service, Swiftcourt Secure Escrow Payment. This gives you the security of a payment solution that helps transfer the money from buyer to seller via an escrow account that holds the purchase sum safely until the handover is confirmed by both parties. Click here to read more about Swiftcourt Secure Escrow Payment

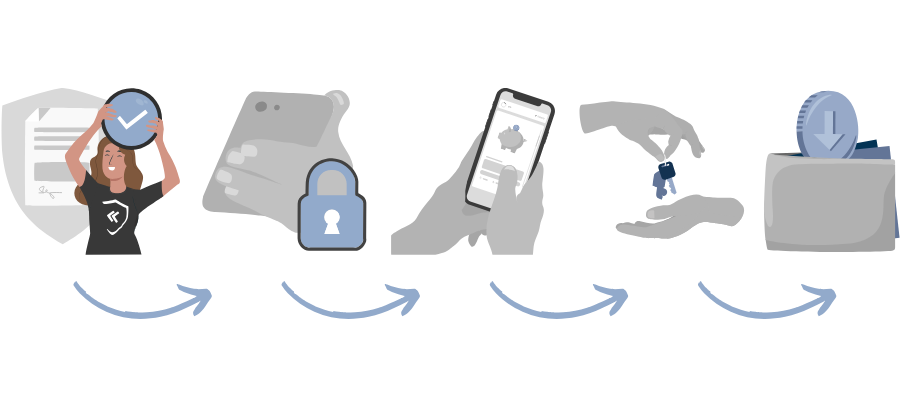

How it works

- Digital Contract

The buyer and seller agree on the terms of the transaction, sign a contract and decide to use Swiftcourt Secure Escrow Payment. - The seller connects their bank account

The seller completes an AIS and chooses the bank account they wish the purchase sum to be paid out to once the payment is complete. - The buyer sends the Purchase Sum to the escrow account

The buyer transfers the purchase sum via our online banking provider into an escrow account held by a trusted third-party escrow agent. - You both confirm the handover

Both parties fulfill their side of the agreement. For example, the seller ships the goods, or the handover is completed successfully. - The seller receives the money

Once all conditions are met, the funds or assets are released to the seller. If the conditions are not met, the funds may be returned to the buyer, or the dispute may be resolved through further negotiation or legal means.

Unlike traditional transaction methods, we offer you more security since we've built our payment service to cover gaps in payment structures that fraudsters like to exploit.

When the purchase sum is transferred to the escrow account, the buyer can no longer access it. As the sum has not been paid to the seller either, we have eliminated all risks that might occur during a purchase between private individuals.

A simple but effective way. As mentioned above, the purchase sum remains in the escrow account until both parties confirm the successful handover.

In short, we’ll relieve you of the stress of the process.

One of our many contracts where we offer Swiftcourt Secure Escrow Payment is in our Car Sales Agreement Contract. When you use our contract combined with the Swiftcourt Secure Payment you’ll never have to worry about the seller running away with the vehicle after you’ve transferred the money and as a seller you’ll never have to worry that you won’t get paid. If you want to be even more prepared for buying or selling a used car, click here to read our Blog post about Buyers & Sellers Guide to Vehicle Purchase Agreement.

Conclusion

Open banking is reshaping the financial services industry by promoting transparency, competition, and consumer empowerment. With its ability to offer more personalized financial products and enhance access to financial services, it has the potential to transform how consumers manage and interact with their finances.

At Swiftcourt, we have adapted the Open Banking process and combined it with an escrow account to provide maximum security for buyers and sellers. When you’re using Swiftcourt Secure Escrow Payment we act as a third party in your transaction and make sure that the seller receives the payment and the buyer gets the product. Our goal is to make private transactions safe, smooth, and secure. It’s made with private parties LIKE YOU in mind.